Rare Earth Elements (REEs) are a group of 17 chemically similar metallic elements that have been mined and utilized globally for over 70 years. They are essential raw materials for modern technology, widely used in everything from electric vehicles (EVs) and wind turbines to smartphones, computers, and other high-tech products.

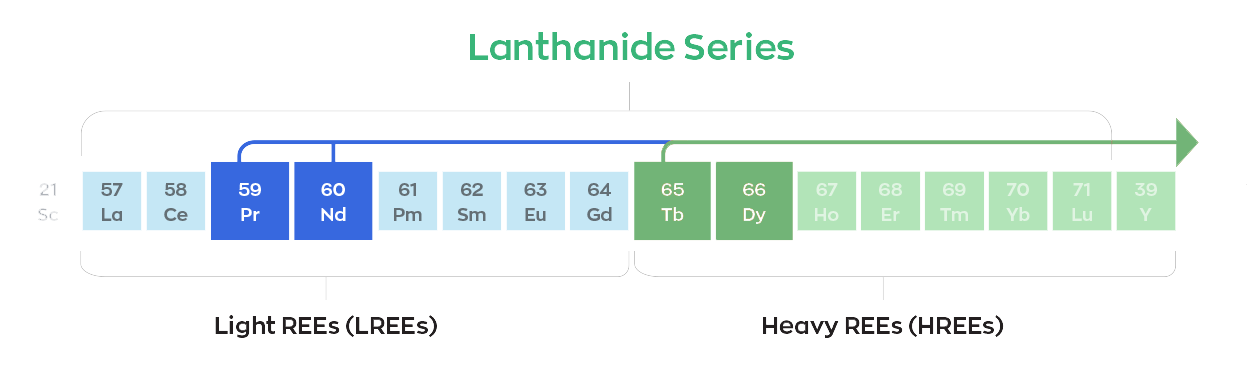

According to the U.S. Department of Energy’s (DOE) 2023 Final Critical Materials List, four REEs are classified as most critical due to their essential role in clean energy technologies and high supply chain risks:

- Dysprosium (Dy)

- Neodymium (Nd)

- Praseodymium (Pr)

- Terbium (Tb)

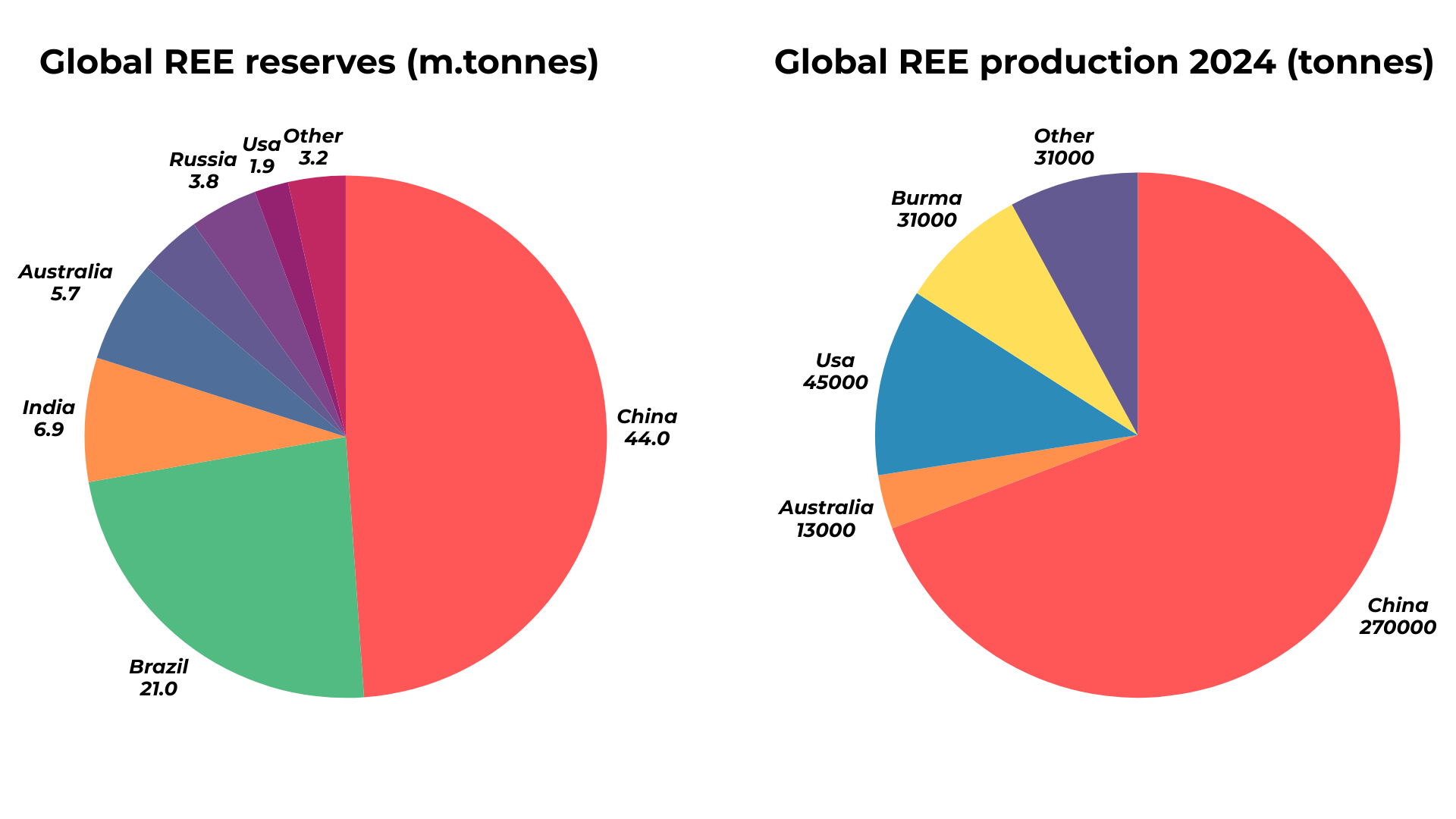

Meanwhile, the European Union’s Critical Raw Materials Act, which came into force on May 23, 2024, designates all 17 rare earth elements as critical, underscoring their importance in industrial and technological applications worldwide.